Context on Biden's LNG Decision

Context on Biden's LNG Decision

On Jan 26, 2024, the President Biden's Administration announced a pause on the permitting of new LNG export facilities. Here's some commentary and an overview of the LNG market.

As always, this is not investment advice: Do your own research.

On September 23, 2022, a series of large, underseas explosions were reported in the area of the Nord Stream pipelines, a major pipeline system connecting Russian gas fields with an energy hungry Germany. We’ll just touch on a few key problems leading up to the pipeline rupture.

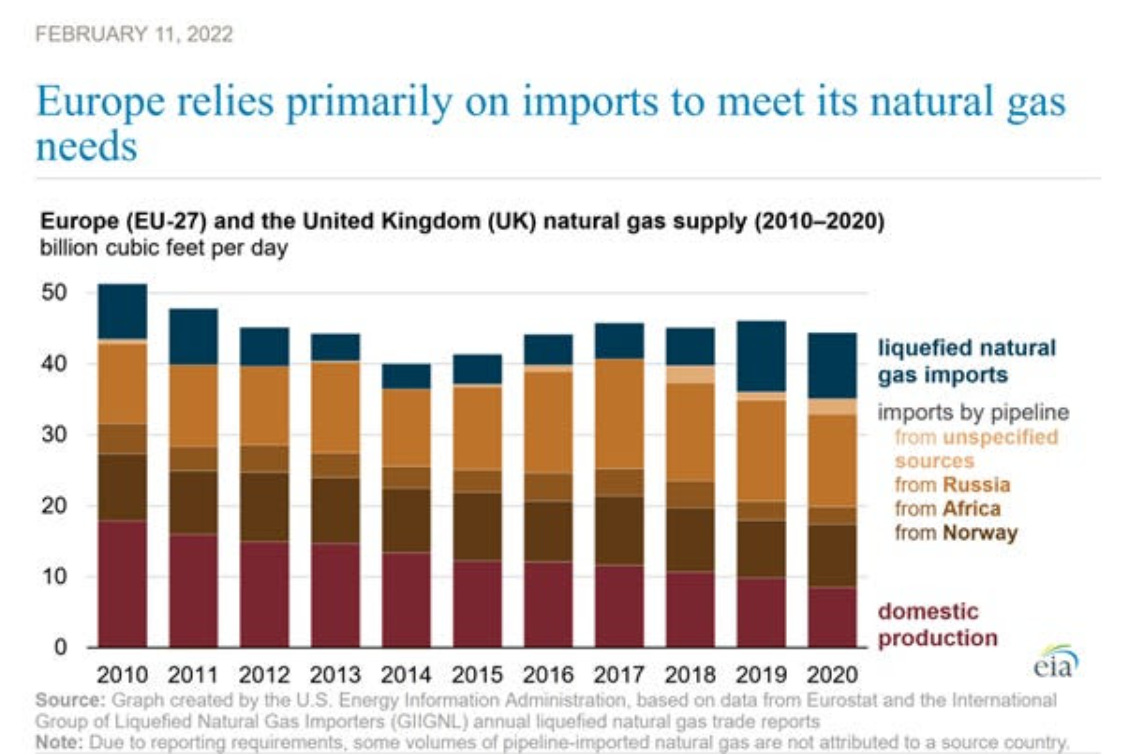

In the years before the explosion, Europe’s leadership was convinced that they were on the cusp of an energy transition away from fossil fuels to a green renewable future. Many European governments blocked or heavily restricted fracking for natural gas, contributing to a long, downward trend of the EU’s domestic production. Instead, the EU greatly increased its dependence of pipeline imports from Russia, Norway, and LNG imports.

For years, there were warning signs that relying on Russia was a bad idea. Since the fall of the USSR, Russia demonstrated a long history of turning off or threatening to stop gas flows to Europe. In 2009, Gazprom shut off gas flows to Ukraine during a financial dispute. Russia also reduced or threatened gas flows in the 1990s, 2013-2014, and again in 2015. Yet that little thing called ‘energy security’ was not allowed to get in the way of the green utopia.

Then as Europe recovered from the 2020 Covid lockdowns, a wind drought hit the continent in 2021. Exceptionally low wind speeds caused wind turbine output to plummet. CNBC reported in September of 2021 that “Energy giant SSE said its renewable assets produced 32% less power than expected between April 1 and Sept. 22 thanks to historically dry and low-wind conditions.” This combination of wind drought and economic recovery drove European gas prices up in 2021.

Then came the Russian invasion of Ukraine of 2022. Europe responded by sanctioning Russia, one of its primary oil and gas suppliers. Europe threatened to punish Russia….by mandating that Russia sell energy to Europe at a discount (AKA a price cap).

Ironically, Russia had trouble delivering gas to Europe.

By July 2022, Russia’s Gazprom announced a Force Majeure (An act of God preventing one from fulfilling a contract), claiming that the sanctions and other issues out of its control forced Russia to stop gas deliveries. Germany’s largest gas importer from Russia (Uniper) rejected the Force Majure, asserting that Russia was still obligated to deliver gas.

Following close after the rejection of the Force Majeure, CNBC reported on Sep 8, 2022 that Russian’s President Putin stated:

“Will there be any political decisions that contradict the contracts? Yes, we just won’t fulfill them. We will not supply anything at all if it contradicts our interests.”

“We will not supply gas, oil, coal, heating oil — we will not supply anything…We would only have one thing left to do: as in the famous Russian fairy tale, we would let the wolf’s tail freeze.”

Later that month, the Nordstream pipeline ‘blew up.’ What we lacked in solid evidence was made up in a buffet of accusations: you could find whatever theory you wanted in this high-stakes game of Clue: Russia blamed the West; some in the West blamed the West; others blamed Russia, Ukraine, China, or a terrorist group.

Yet while the pundits pointed fingers, Europe faced an extreme energy crisis, had the winter of 2022/23 been cold. Fortunately for Europe, the winter was mild, and Europe was able to import vast quantities of US LNG (liquified natural gas: natural gas made extremely cold, -260F, so it will turn into a liquid for transport.)

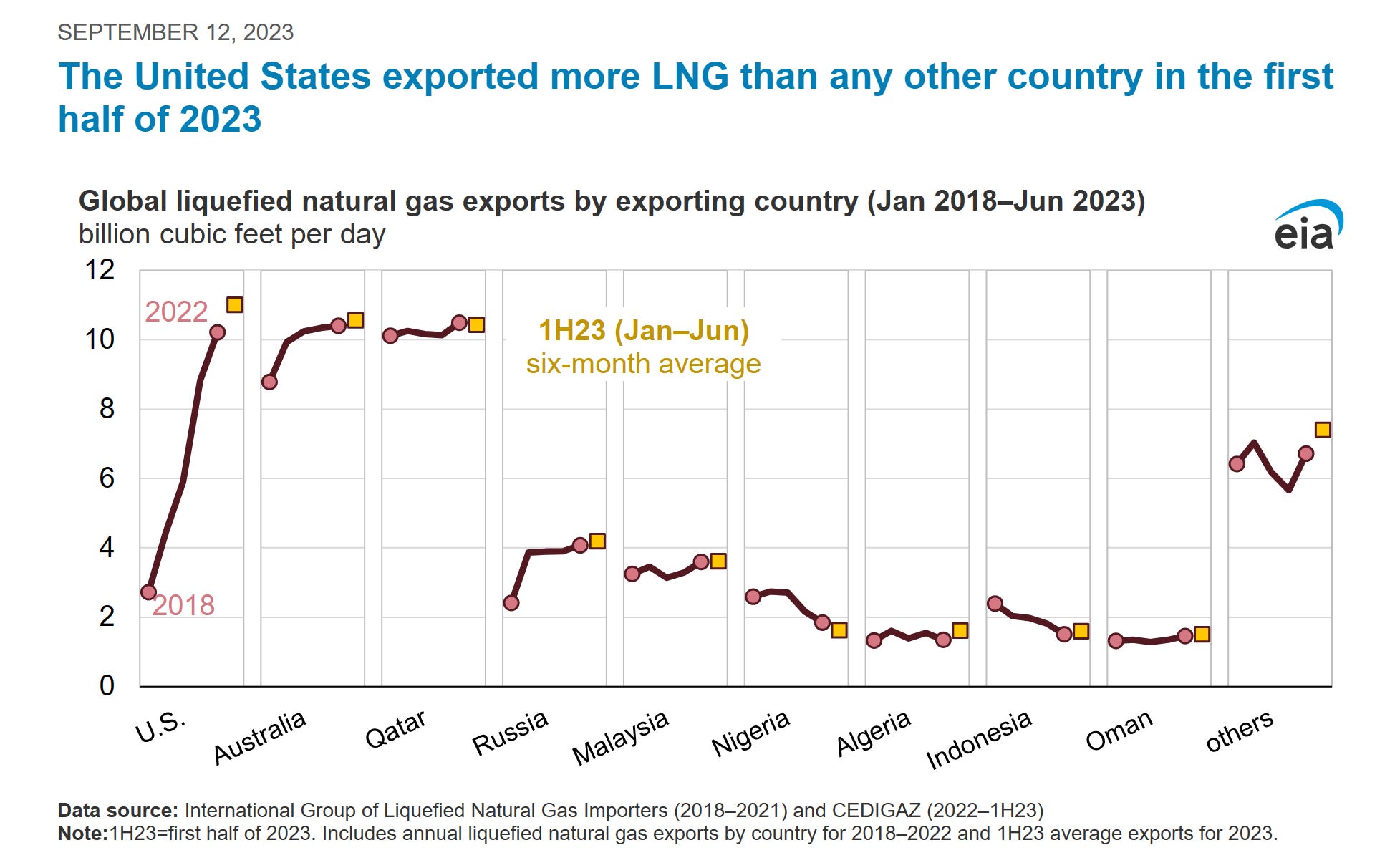

In that crucial year of 2022, the US supplied 43% of Europe’s LNG as Europe scrambled to replace Russian gas.

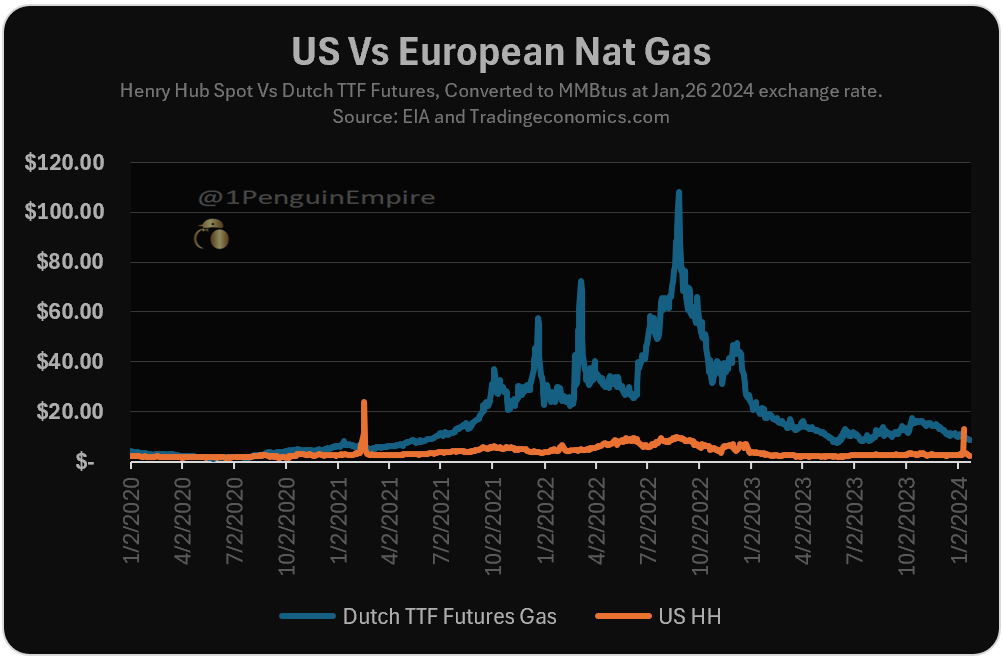

Yet it came at a price. As you can see, at the peak of the crisis, Europeans were paying more than 10x the price for the same molecules of gas that you could get in the US. One of the challenges in comparing US to European gas prices is that they tend to be quoted in different measures. To make it easy to compare, here’s a chart of both US and Dutch TTF futures prices, converted into the same units for comparison.

This is a good time to say thank you to all the roughnecks, and landowners in places like Oklahoma, Texas, Pennsylvania and countless other places, and to those financiers, business owners, chemical plant workers, and engineers who bucked the ESG trend to divest from oil and gas. Had the US followed Europe’s green template and banned or discouraged fracking and LNG exports construction in the US, it would be a very different and far darker story.

But that only is a recent development. Over the past decade, the United States has gone from a non-existent player in the LNG export industry to now the largest global LNG exporter.

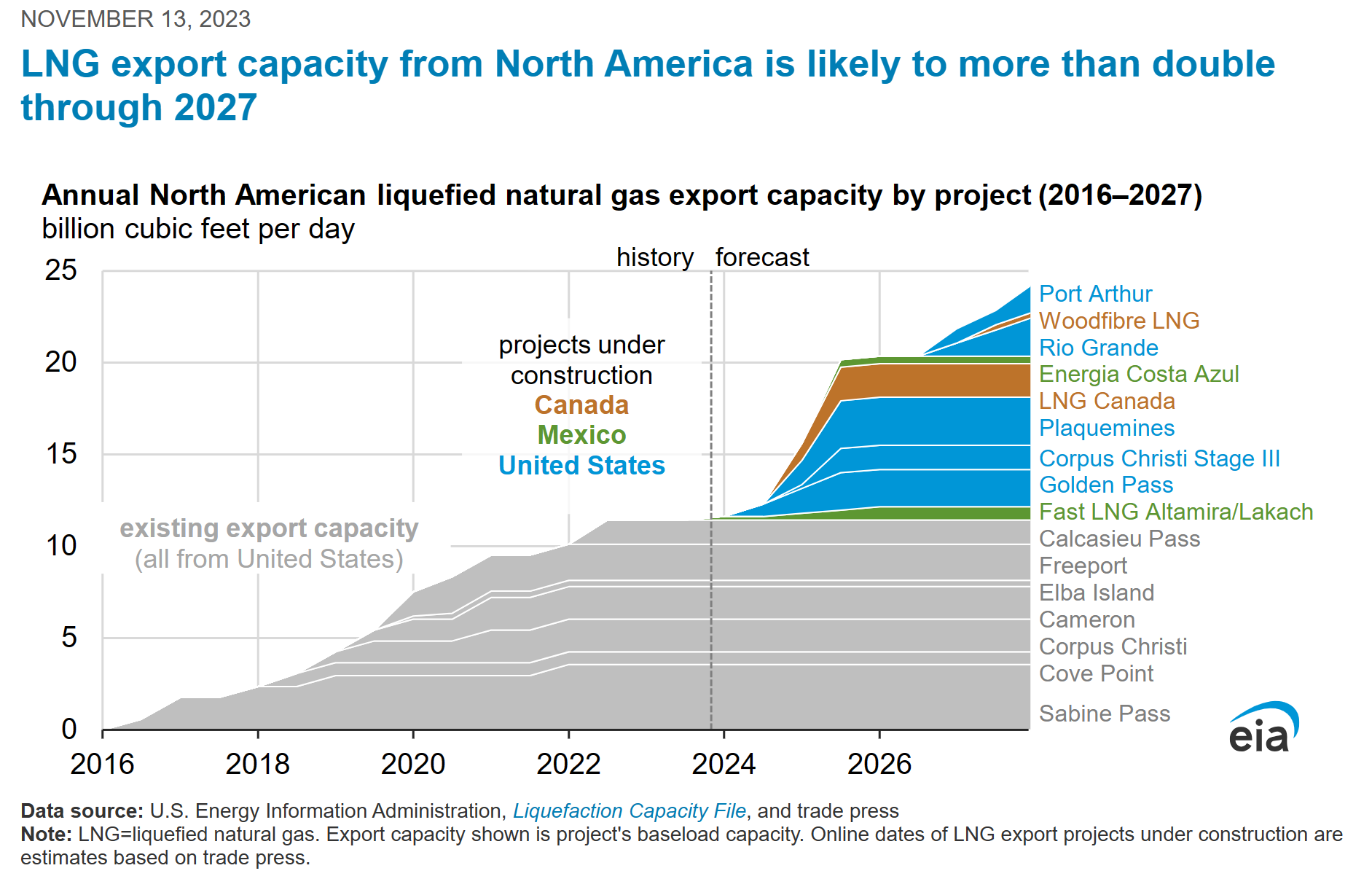

As of November 2023, the EIA forecasted that North America’s LNG export facilities would more than double by 2027, with most of that capacity coming from the US.

Yet much of that capacity is/ or would have come online after 2022.

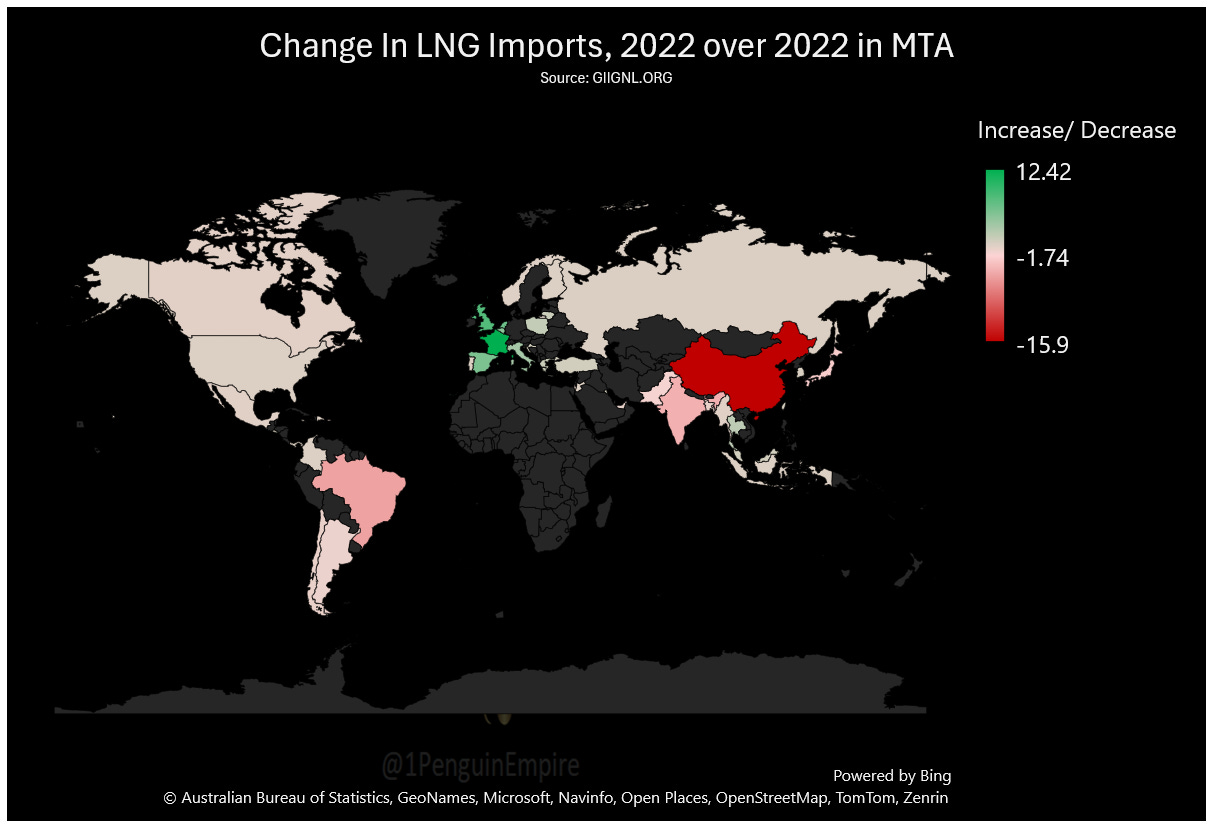

In 2022, the global markets could not bring enough supply online to meet both Europe’s increased demand and existing global demand. In 2021, Europe imported around 75mta (million metric ton/annually) of LNG out of a global market of ~373mta. Yet in 2022, Europe imported a whopping 120mta from a global market of ~ 390mta in 2022. The market only expanded ~17mta but Europe’s demand when up ~45mta.

To get through 2022, Europe simply outbid much of the rest of the world. When prices skyrocketed, Asia reduced imports by over 20mta and Brazil reduced its imports by over 5mta, according to GIIGNL’s 2023 Annual Report. Note, that for much of 2022, Germany didn’t have major LNG plants online. Despite the war and the energy crisis, environmentalists still protested Germany’s decision to expedite bringing LNG terminals online.

The energy world is a bit like a balloon. If you squeeze one part, another part of the balloon starts to budge. While Europe was soaking up every molecule it could, Asia refocused on coal. In 2022, coal production rose, reaching new all times records as Asian countries decided that coal was probably better than LNG imports that Europe could outbid. For example, in Feb of 2023, Pakistan announced that it was going to increase its coal capacity by 4x while no longer adding natural gas power plants.

As

has documented, China is also heavily investing in coal. He wrote: “On November 27, three days before the opening of the meeting in Dubai, Global Energy Monitor released a report showing that some 204,000 megawatts of new coal-fired capacity is now under construction around the world. Of that 204,000 MW, about 67% is in China. To put that massive amount of new capacity in perspective, the U.S. currently operates about 205,000 MW of coal-fired power plants.”

And that brings us to now….

On Jan 26, 2024, in an attempt woo green voters (and one might wonder if it’s designed to distract from the unfolding saga in Texas), the Biden Administration paused new permits for LNG export terminals. According to the White House Press release:

“President Biden has been clear that climate change is the existential threat of our time – and we must act with the urgency it demands to protect the future for generations to come. That’s why, since Day One, President Biden has led and delivered on the most ambitious climate agenda in history, which is lowering energy costs for hardworking Americans, creating millions of good-paying jobs, safeguarding the health of our communities, and ensuring America leads the clean energy future.

”Today, the Biden-Harris Administration is announcing a temporary pause on pending decisions on exports of Liquefied Natural Gas (LNG) to non-FTA countries until the Department of Energy can update the underlying analyses for authorizations.

And while the White House promised that this pause would not impact short term LNG, they added this bit:

“As Republicans in Congress continue to deny the very existence of climate change while attempting to strip their constituents of the economic, environmental and health benefits of the President’s historic climate investments, the Biden-Harris Administration will continue to lead the way in ambitious climate action while ensuring the American economy remains the envy of the world.”

The press release continues, proudly boasting of the “Biden-Harris Administration’s Top Climate Accomplishments” included that the administration:

Signed into law the largest climate investment in history, the Inflation Reduction Act

Launched the American Climate Corps

Canceled remaining oil and gas leases

Signed an Executive Order that sets an ambitious target to make half of all new vehicles sold in 2030 zero-emissions, while proposing strongest-ever limits on tail pipe emissions

Proposed carbon pollution standards for coal and gas-fired power plant emissions that would avoid hundreds of millions of tons of carbon dioxide emissions and protect people’s health

Accelerated permitting of clean energy projects

To be clear, the US will continue to have a large export capacity. This is a ‘pause’ on new project permits. But it’s very obvious that the current President is openly playing favorites. Perhaps the market is overbuilding supply, but it’s astonishing to watch the administrative state make- or pretend to make- that decision by fiat.

Even if the Biden Administration (or the next administration) reverses this political ban and green lights future LNG buildout, the Biden Administrations decision creates uncertainty for both investors, and leaders in the developing world.

As always, thanks for reading!

And yes, it’ll impact Texas. Not to speculate on the motives, but it looks bad on its surface.

But it brings up a fundamental issue: the ‘social cost’ of GHG is allegedly the justification. Really, it’s can be extremely easy to get wildly distorted imagined costs that can ‘justify’ shutting down just about anything.

Thanks for the restack!