Drill, Baby, Drill?

“Show me the incentives and I’ll show you the outcomes.” - Charlie Munger

Will a Trump administration drive down the price of oil? To help answer that question, it’s time to strap on your boots, step into the oil patch, and ask yourself:

“If I was the one paying for a new oil well, would I make the leap and “drill, baby, drill,” or would I let that well sit untapped?”

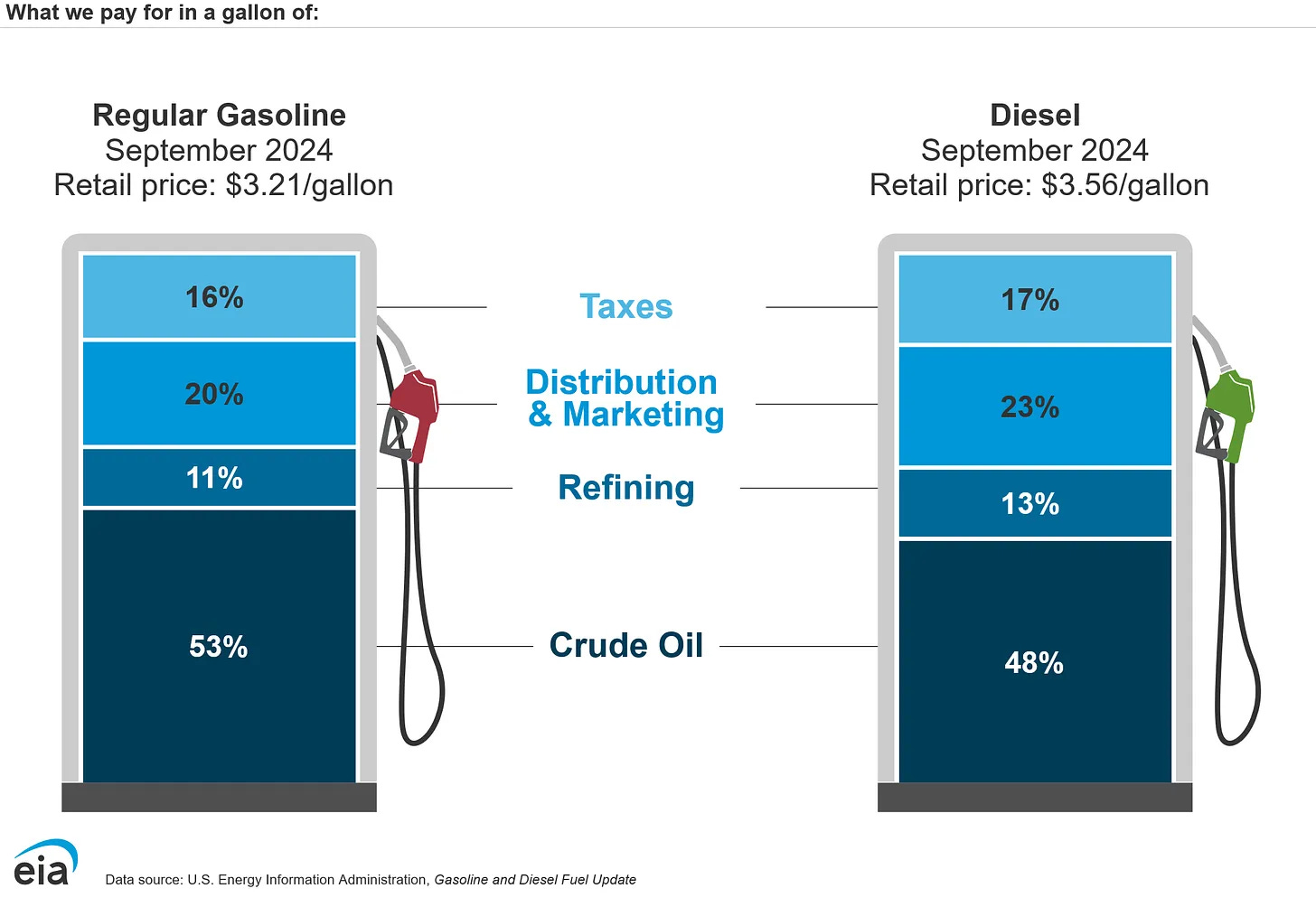

When we talk about the price of oil, what we’re usually talking about is the price of gasoline. It’s posted everywhere and it matters to almost everyone. And when prices go up, Presidential approval ratings tend to go down.

Gasoline prices are driven by the price of crude oil, which accounts for around half of what Americans pay at the pump. But here's the kicker: oil demand is inelastic, meaning it’s hard for us to cut back on demand. Yes, gas going from $2 to $3 a gallon is a 50% increase and it hurts our wallets - but it doesn’t mean we cut our driving by 50%. Because of that, a small supply shortage can send prices sky high. On the flip side, an oversupply can send prices plummeting. So, when the price goes up or down, it can indicate that the markets are undersupplied or oversupplied.

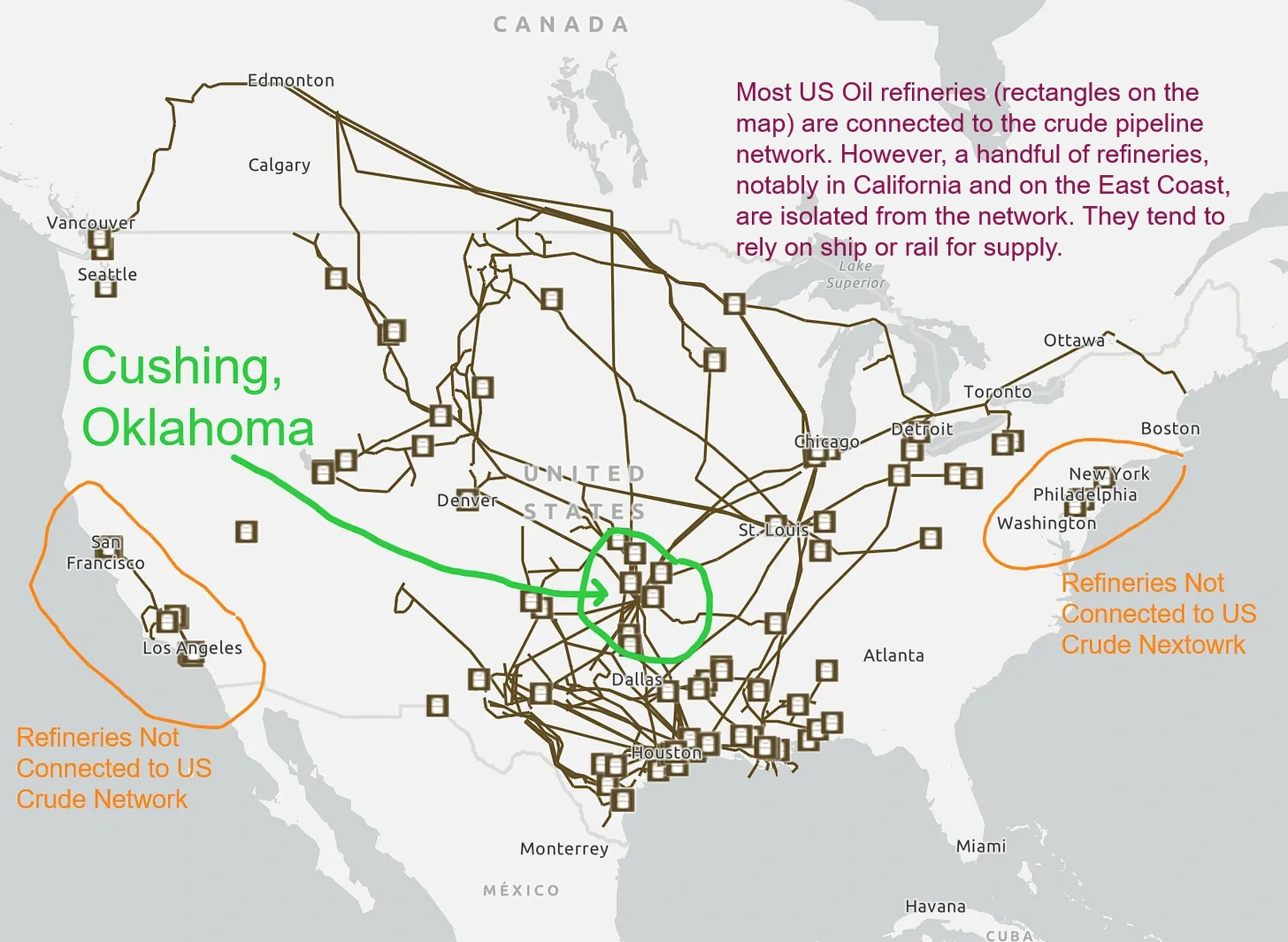

A measure of that supply is the price of oil in a little town few have heard of. Cushing, Oklahoma might only have around 8,400 residents, but nearly two dozen major pipelines converge there, making it the crossroads of North America’s oil industry. In fact, Cushing is the physical delivery point for West Texas Intermediate (WTI) crude oil, a benchmark reference price used throughout the US and Canada.

During the first Trump administration, WTI prices generally floated in the $50-70 range. But for reference, $60 a barrel in 2019 adjusted for inflation is now worth around $74 in 2024.

Prices nosedived during the COVID-19 panic. Yet by 2022, WTI surged to $114+ in the wake of the recovery and Russia’s war in Ukraine. By the spring of 2024 it was around $80-85. And at the time of this writing, it was dancing around $67-70.

What Trump Can and Can’t Do

It almost goes without saying but California probably isn’t going to have an oil boom anytime soon, regardless of who's in the White House. The US is a federal system, with states having significant local control.

But Trump could still pull key federal levers.

Recently, Trump announced that Elon Musk and Vivek Ramaswamy will lead a newly formed Department of Government Efficiency, designed to radically reshape, reform, and downsize the federal bureaucracy. Musk and Ramaswaym published a piece in the WSJ outlining their plans. Here’s a quote (emphasis added):

“Our North Star for reform will be the U.S. Constitution, with a focus on two critical Supreme Court rulings issued during President Biden’s tenure.

“In West Virginia v. Environmental Protection Agency (2022), the justices held that agencies can’t impose regulations dealing with major economic or policy questions unless Congress specifically authorizes them to do so. In Loper Bright v. Raimondo (2024), the court overturned the Chevron doctrine and held that federal courts should no longer defer to federal agencies’ interpretations of the law or their own rulemaking authority. Together, these cases suggest that a plethora of current federal regulations exceed the authority Congress has granted under the law.”

Bravo and well said!

Just to see how vast the US Federal Government is, I went to ai.google.com and asked “How many US Federal Government agencies are there?” Basically, as Musk pointed out in a recent podcast, we don’t know:

Specifically, a Trump administration could reign in the EPA’s warpath against internal combustion engines, coal and natural gas power plants. As the Energy Bad Boys pointed out in a fantastic piece here, the current EPA’s power plant policies are effectively driving the grid off of a reliability cliff. Big changes may be coming…

And to top it off, a Trump administration would likely be far more friendly to interstate and large scale oil and gas infrastructure projects such as new pipelines and LNG export facilities.

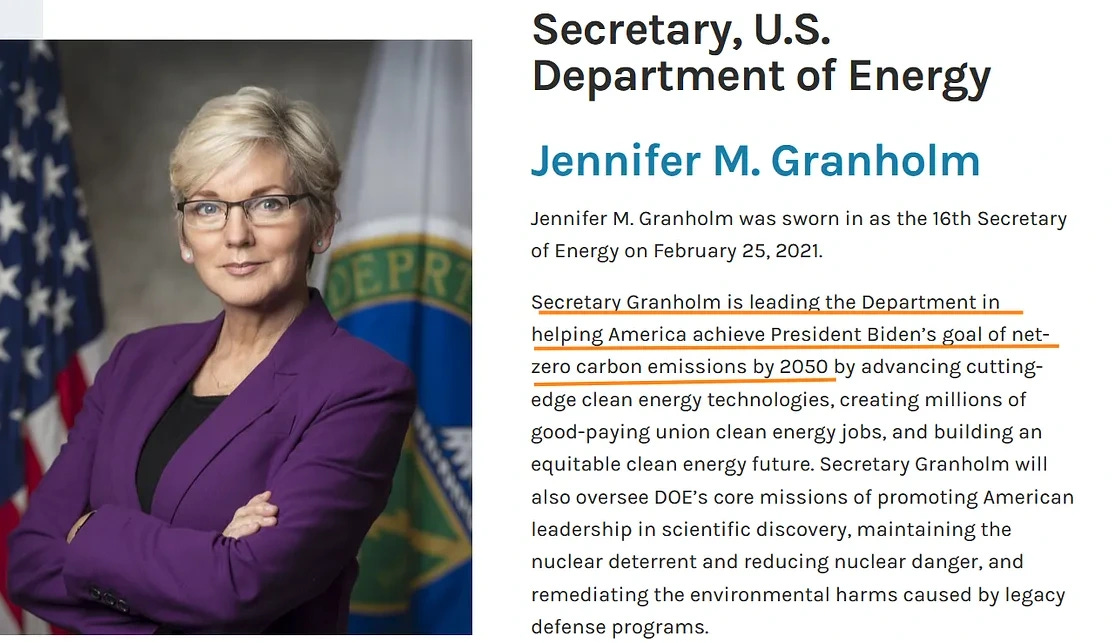

To understand the difference in policies, look no further than the Department of Energy. President Biden’s energy secretary - Jennifer Granholm - is a lawyer who believes the US Military should adopt electric vehicles. She also thinks her job is to shepherd the US towards Net Zero by 2050. Here’s her bio from the US department of energy’s website.

In contrast, Trump’s pick for energy secretary, Chris Wright, is the CEO of a fracking company. He is vocal about the need to increase U.S. energy supply to fight global energy poverty. His company even went as far as to publicly declare, “There is No Energy Transition” in a recent investor presentation.

What a change in direction. Yet… Can Trump boost oil production?

Let’s now put ourselves in the boots of a real (hypothetical) oil producer. Imagine you’ve come into a nice inheritance and you’ve decided to start your own oil company. Let’s look at some of the hoops you’d have to jump through (this isn’t investment advice).

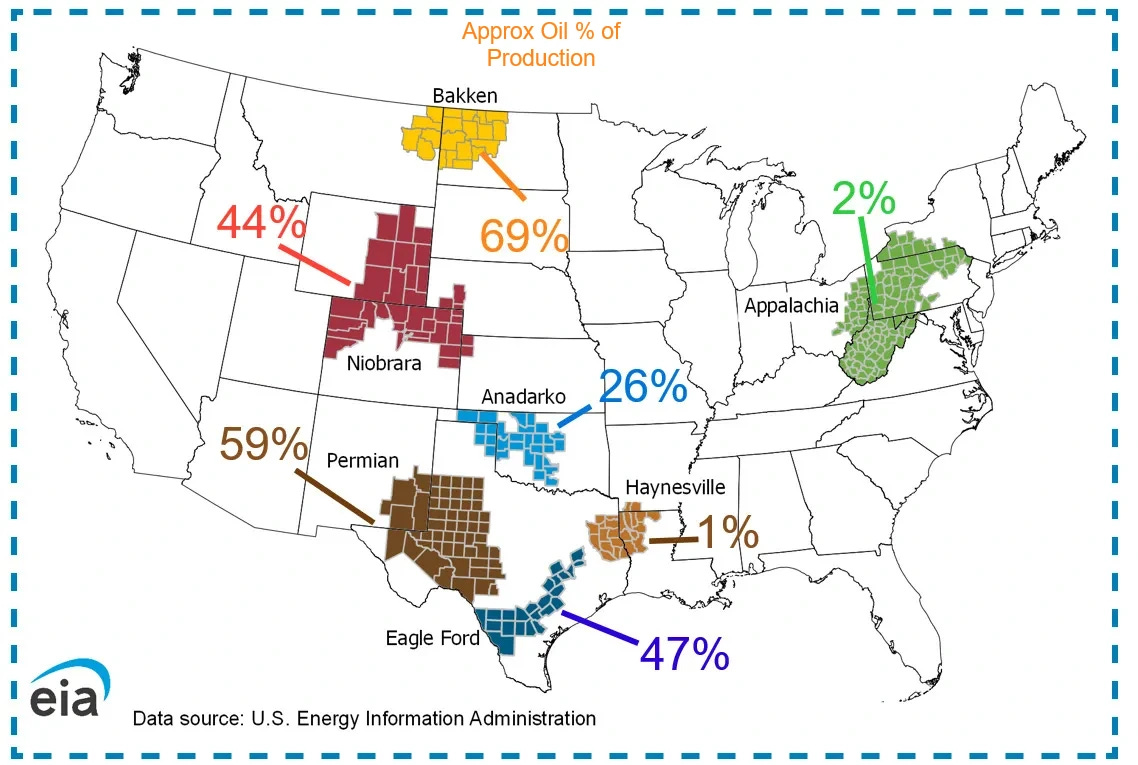

You first need to do your homework and find the right rock - It’s all about the rock. Some rock is rich in oil and gas, while others aren’t worth the squeeze. Where you drill can have a big impact on what you produce. Here’s a map from the EIA, with oil as a % of the region’s average production for major shale basins. In Appalachia, the price of natural gas can make or break drilling. But in the Permian, oil is king.

Even within a region, you still need to know exactly where to drill. Rock is layered. You might drill down 10,000 feet and find oil, but if you only drill down 9000 feet, you might come up dry all together.

To help narrow down where to drill, you’ll not only look at geological maps, you’ll also study well logs of nearby wells. Oil companies put equipment down existing wells to take all sorts of readings. Those readings - compiled into well logs- provide clues. For example, oil tends to offer more electrical resistance than brine. If you’re reading a well log and you see a spike in electrical resistance, that might be a clue.

After you find the right spot, it’s time to haggle for mineral lease rights. Securing mineral leases can cost anywhere from hundreds to tens of thousands of dollars per acre, depending on the area, the price of oil, and if those leases have wells on them. In the oil boom in the late 2010s, it wasn’t uncommon to see prices of $10,000 to 20,000 per acre for prime spots in western Oklahoma. The Permian in Texas even saw prices as high as $55,000 to $76,000 per acre.

Getting a lease isn’t cheap, especially when you consider that oil wells are often drilled horizontally for 2, 3, and even 4 miles. You might need a few thousand acres to set up shop. Another option is to partner up with an existing company that already holds leases to split both the costs and profits.

Once you’ve secured the lease and permits, it’s time to plan the infrastructure and surface rights for the well pad and other equipment. Plus you’ll need to negotiate with a natural gas processing plant. Crude can be transported vast distances before it’s refined. Natural gas is a different story and it generally needs to get processed locally to remove water vapors, CO2, contaminants, and valuable products like butane and propane.

I’ll pause here to say that getting to this point take a F$^! ton of work, determination, money, skill, and some luck. And we haven’t begun to drill for oil yet.

Now’s the big question: how much does it cost to drill an oil well? It depends on:

How deep the well is

How difficult the rock is to drill and frack

How much of the resource do you want to drill.

Today, most wells are drilled sideways through a layer of rock, sometimes for 10,000, 15,000, or even 20,000 feet. In late 2024, it’s not uncommon for companies to report that it costs $800 to $1100 per horizontal foot to drill and complete a well. So, a 10,000 foot oil well could cost $8–11 million in Oklahoma or Texas.

And what could that investment get you? Here’s where things get tricky.

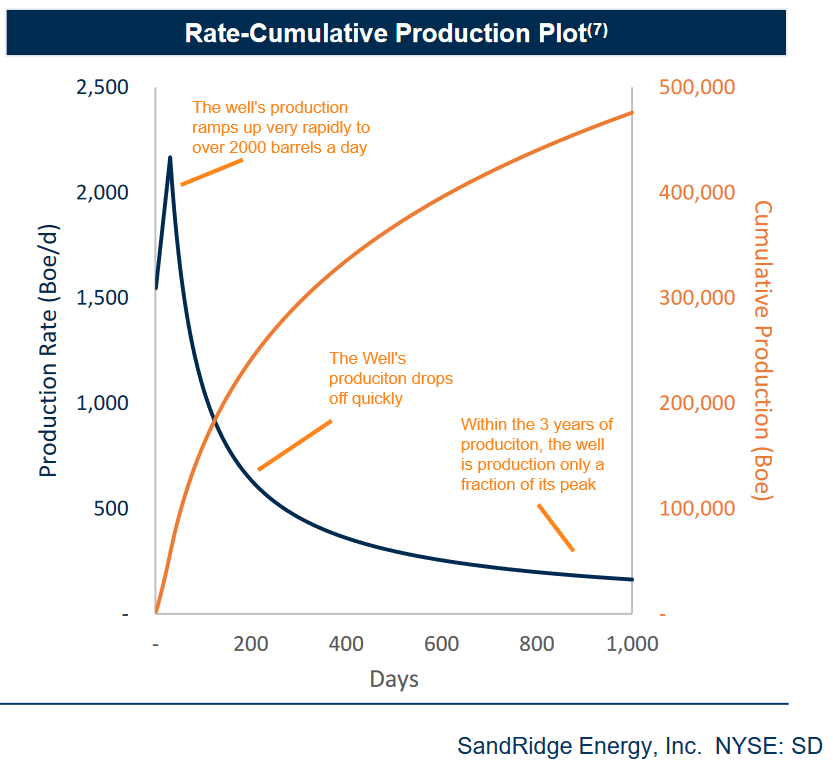

We’ll turn to Sandridge Energy (not investment advice and I do not own). Let’s take a look at their planned drilling operations in Western Oklahoma. Here’s a screen shot from their investor presentation with commentary added.

This is the “average” production Sandridge expects from top tier new wells in the area.

Most shale wells have the same pattern: a quick ramp up, followed by a rapid decline. In Sandridge’s example, their top new wells are estimated to average around 500,000 barrels in the first 1000 days online. But those barrels aren’t pure oil.

Remember that oil tends to get produced with gas, propane, butane, and other liquids. So, at $67 per barrel of oil, you might only get $40-45 per barrel of production, depending on the mix. And that’s before royalties, operating costs, and taxes.

Royalties are among the biggest expenses. Yes, you might have spent an arm and a leg leasing the mineral rights, but now it’s time to pay Farmer John a ‘commission’ for the production on his ranch. In Oklahoma, royalty rates tend to run around 18-20%.

Now its time to pay our own expenses. Based on fall 2024 numbers, those expenses run around $10-15 a barrel and include:

electricity for the well pump

disposing the brine water produced

transporting the oil

natural gas processing fees

administrative costs

taxes on production

Can You Make Money?

After all of the expenses, you might only get $20 to $30 per barrel. If your well only produces 500,000 barrels in 2 or 3 years, is it worth a $10 million investment? Or should you park that money in bonds, safely earning 5% a year?

This is the decision oil and gas producers face: If oil prices drop into the $60s, producers need to decide if they should drill, and if so, they might become very selective on where to drill.

Federal Reserve Survey

Let’s turn to the Federal Reserve Bank of Dallas’ survey of oil and gas producers. According to the oil companies, they need oil ~ $60s to keep drilling. Now this doesn’t mean they’ll completely stop drilling, but it does mean they’ll only drill the best locations if oil is $60, limiting overall drilling.

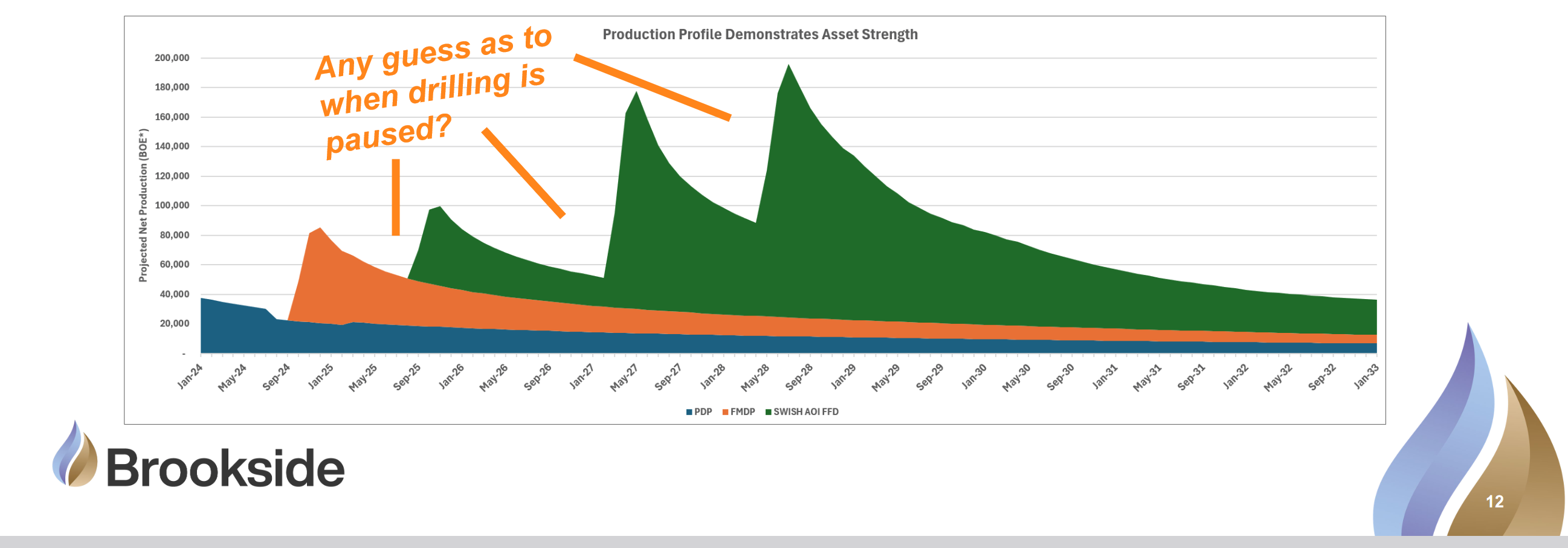

What happens to oil production if people cut back on drilling?

If you rapidly stack drilling, you can ramp up production. But if you stop drilling….

Here’s a screen shot from Brookside Energy, a small startup drilling in Oklahoma (not investment advice). Here’s what they think their production will look like over the next few years. It’s pretty obvious to see when they plan to drill, and when they aren’t drilling.

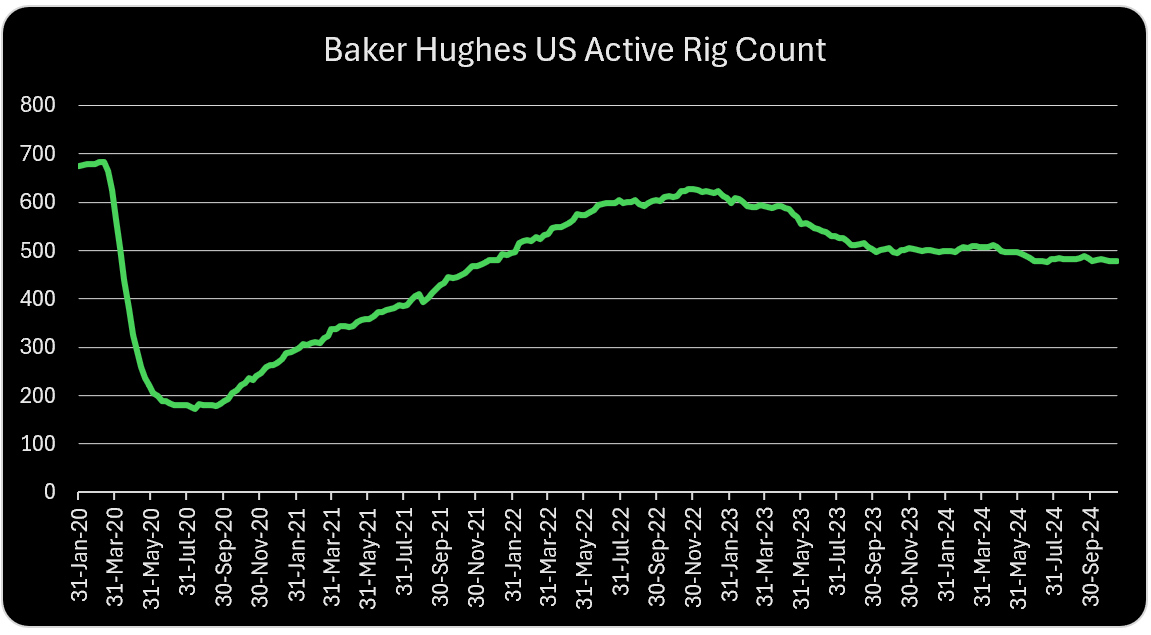

We’ll leave you with one last chart: Baker Hughes’ OIL rig count. When oil prices boomed after COVID and the war in Ukraine, producers aggressively drilled. Yet, when oil prices dropped, the number of active rigs declined.

In closing, a Trump administration just might bring some much needed changes to US Energy policy. But would you “drill, baby, drill” if your money was on the line? It all depends. If Trump’s business-friendly reforms usher in economic growth, we’d definitely need a lot more drilling if oil prices go up with demand. The same could be said of natural gas. Increased electricity demand from AI, manufacturing, and increased LNG exports could incentivize drilling for natural gas even if oil remains flat. However, if oil floats in the $60s, and if natural gas prices don’t rise, there’s not much incentive for most producers to mount a large scale drilling campaign.

That’s all for now! Thanks for reading!

Thanks for a nice overview. A couple other aspects may be worth mentioning.

A big aspect of what the Feds do control is permitting on federal lands. But companies obtain permits long before drilling, and they actively manage their permitting activity in response to changes in policy. So a lot of permits were stockpiled during Trump's first term but only drilled later, giving some uninformed commentators the impression that Biden was the "drill baby drill" president.

Another aspect is that technology has improved and will improve. The producers are getting more production per rig and so also lower costs. This led to some recent increases in production that surprised analysts. There may someday be an increase in cost per barrel due to resource depletion. But not yet. (Costs have also dropped by staggering amounts in the oil sands in Canada.)

Fantastic, thanks lads. It's always interesting talking with folks about how oil prices are derived, the break even price for it, exploration research costs and the speculative plunge companies must take to possibly reap the rewards of a field. If this primer was read widely it would help make everybody a little smarter about energy.

As far as net cost calculations for profitability are concerned, Wright and co. will streamline federal regulation and thereby reduce upstream costs for oil producers. Everyone's least favorite crone librarian, Granholm packing her bags is clearly a boon for exploration, production, and refining.