The Spartan Way

"Zero to five and out" - Richard McHardy on buying quality undeveloped or under-utilized oil & gas properties, improving them, then selling them for a profit.

Disclaimer:

This is not investment advice. Consult your own financial professional. This piece is opinion only and reflects some of the internal research at PenguinEmpireReports. This is NOT a comprehensive overview of the company, its risks, the management, and the industry. Picking individual stocks is risky and may be subject to fraud, loss of investments, bankruptcy, and other risks such as a crash in commodity prices.

This is NOT an endorsement or a solicitation for the purchase of Logan, Spartan Delta, or Crescent Point shares. Currently, PenguinEmpireReports does not hold any position in those companies. This may change at any time without notice.

KNOW WHAT YOU OWN.

As they say, history does not repeat itself; but it does seem to rhyme. And while past performance is not a guarantee of future success, it is a useful starting point.

The Spartan team favors buying underused or undeveloped oil and gas assets in Western Canada. Armed with technical knowledge, the team builds up the new assets, often merging them with other additional buys. When production and cash flows increase, the assets are sold off. Then, it’s ‘rinse-and-repeat,’ usually with a new startup or a spin-off. For them, this is The Spartan Way.

In July of this year, Spartan Delta announced a major repositioning. Before the repositioning, Spartan Delta averaged production of roughly 70-80K barrels of oil equivalent per day (BOE/D). The realignment split the company into three pieces:

The Spin-Off : Logan Energy Corp, with ~ 4.5K BOE/d and ~ 193k Montney acres

Sold ~36K BOE/d producing assets to Crescent Point Energy for C$ 1.7B

Retained the remaining Deep Basin assets with ~39K BOE/d and ~ 130k acres

But this was just the latest in a long line of Spartans.

The Group of Four

Spartan Exploration was formed in 2008. Early on, a group of four individuals held key positions in Spartan Exploration. That same group held key positions throughout the Spartan franchise, including the new Logan Exploration.

Richard McHardy, CEO of the new Spartan Exploration, started his career as a young lawyer in Calgary in the 1990s and early 2000s. Small oil and gas companies made up a large portion of his client base, offering McHardy the opportunity to learn from the “the best of the best.” When he left his law practice, McHardy founded Titan Energy in 2004. In 2008, Canetic Resources Trust purchased Titan.

Fotis Kalantzis, the VP of exploration, earned a string of degrees including a Phd. in Geophysics and a Masters Of Science in Physics. He held technical positions at numerous companies, including well known firms such Saudi Aramco, Suncor Energy, and Mobil Oil (later Exxon Mobil).

Both Donald Archibald and Rignald Greenslade served on the board at Spartan Exploration, various other positions, and now serve on the board of Logan Energy.

Spartan Exploration is Formed

In 2008, Spartan exploration was formed. By early March of 2008, the company raised just over C$ 4 million through a private placement. Then, the company issued a loan for approx $964,813 so its members could purchase shares in the newly created company.

Then it was off to the races. On Wednesday the week after raising the $4million, Spartan entered into an agreement to fund 45.45% of a well for 25% of its production. The well was in the Weyburn area of Saskatchewan, not too far from the US border. By the end of the month, Spartan also purchased rights to a few thousand acres of undeveloped land in southeast Saskatchewan. And the deals kept rolling. More deals; more cash raised, and more drilling. By the end of the year, Spartan has raised north of $17 million and drilled several wells.

Production grew at a rapid pace, bolstered by selective deals. For example, in the middle of 2009, Spartan purchased a shut-in oil asset from Penn West Petroleum for C$ 1.1 million. The company spent C$1.0 million to upgrade and restart production. By the end of that year, it was producing ~135 BOE/d.

In its first Annual Information report (2009), the Spartan team outlined their strategy, stating: “current economic conditions have resulted in decreased industry activity that has created a drop in the cost of services, materials and land” creating opportunities “for increased returns” (emphasis added).

Management continued:

“Spartan’s growth strategy is to:

1. acquire a land position or drilling opportunities to earn significant land positions

2. build an inventory of low to medium risk drilling prospects…

3. efficiently control costs through facility ownership and operation of wells…

4. seek out opportunities where leaseholders have time or resource issues; and

5. manage risk through the geological and technical expertise Spartan has in each of these areas.”

By 2010, the company focused on drilling and optimizing its recently acquired assets. In the second and last Annual Information report, dated March 17, 2011, Spartan reported spending roughly $57.7 million on capital expenditures for drilling, equipment etc. Less than a month later, Spartan Exploration announced the sale of most of its assets for $229 million. At the time of the sale, the company produced roughly 2500 BOE/d, an impressive accomplishment for a company barely 3 years old.

But, the story doesn’t end there.

As part of the sale, Spartan Exploration spun off part of its assets to form...

Spartan Oil.

And not to be outdone, Spartan Oil quickly grew from less than 1000 BOE/d in Q2 2011 to over 4000BOE/d by Q4 of 2012. Cash flows grew from C$2 million in Q2 of 2011 to north of C$ 20 million by Q4 of 2012.

In November of 2012, Pinecrest Energy announced an agreement to buy Spartan Oil in exchange for shares in Pinecrest. But the honeymoon didn’t even begin for Pinecrest. Before the deal was sealed, Bonterra swopped in, offering ~$47 million more for Spartan Oil. Bonterra’s offer was a “superior deal.” So, Spartan Oil backed out of the Pinecrest deal, paid $12.5 million in fees to Pinecrest, and sold its assets to Bonterra.

And then came…

Spartan Energy

Created in 2013, it grew from 650 BOE/d to ~23,000 BOE/d in 2018 “through an acquisition and development strategy” involving 11 transactions. After acquisitions, management strove to drive down the operating costs per BOE, from ~C$21/BOE in q4 2014 down to ~C$17 per BOE/d in Q1 2018.

Sound familiar?

During this time, in 2017, Richard McHardy was inducted into the Saskatchewan Oil & Gas Hall of Fame. According to the Hall of Fame website, “Spartan Energy was able to take advantage of the downturn through an aggressive round of acquisitions that dramatically increased its assets.” A year later, Vermillion Energy bought out Spartan Energy for ~ C$ 1.4 billion. It was, as McHardy said, “ zero to five and out.”

Next… Can you guess the name?

Spartan Delta.

History was made on April 20, 2020, when oil futures prices dropped to the negative territory for the first time in US history. Prices dropped as low as -$37.63 a barrel (US$ WTI) due to the panic around Covid-19, the oil glut from lock-downs, and the Saudi/ Russian price war.

Those words from Spartan Exploration’s 2009 strategy couldn’t have been fitting for April of 2020: “The Spartan management team believes that…current economic conditions have resulted in decreased industry activity that has created a drop in the cost of services, materials and land.”

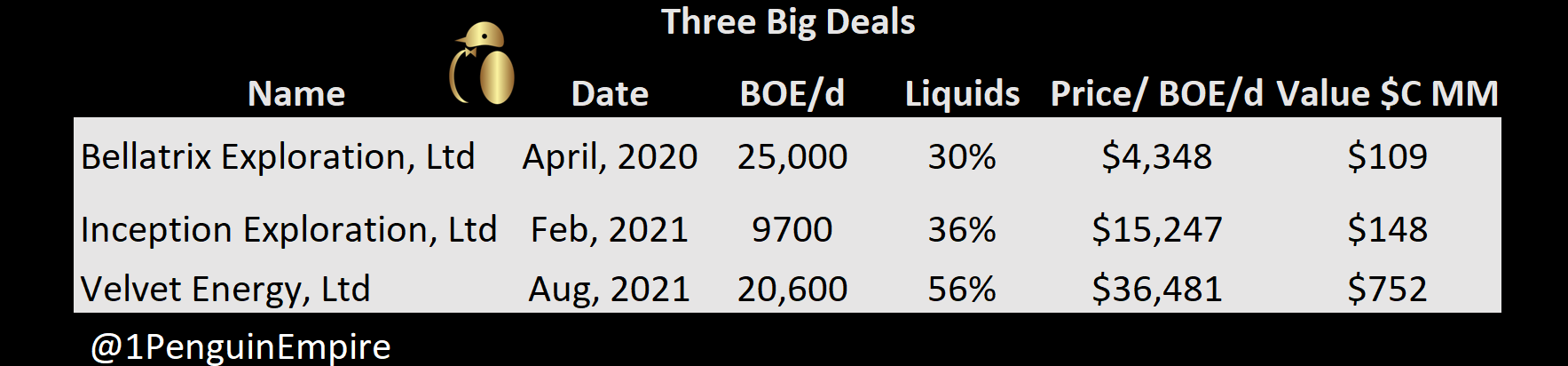

True to form, in April of 2020 (the same month as the negative oil prices) Spartan Delta announced purchased Bellatrix out of bankruptcy. It was an eye-poppingly good deal of ~ C$4,350 per flowing BOE. (As most oil and gas observers know, that is a really good deal. As Kalantzis said in an interview in May 2020, “I probably don’t need to stress (that it’s) something tough to find anywhere else in the basin right now.” And it is still really tough to find anything, anywhere for that price today.

Spartan Delta made two more large deals, acquiring thousands more BOEs/d in 2021. Spartan developed its assets, all while maintaining a pristine balance sheet, with a equity to liabilities ratio of ~ 3:1.1

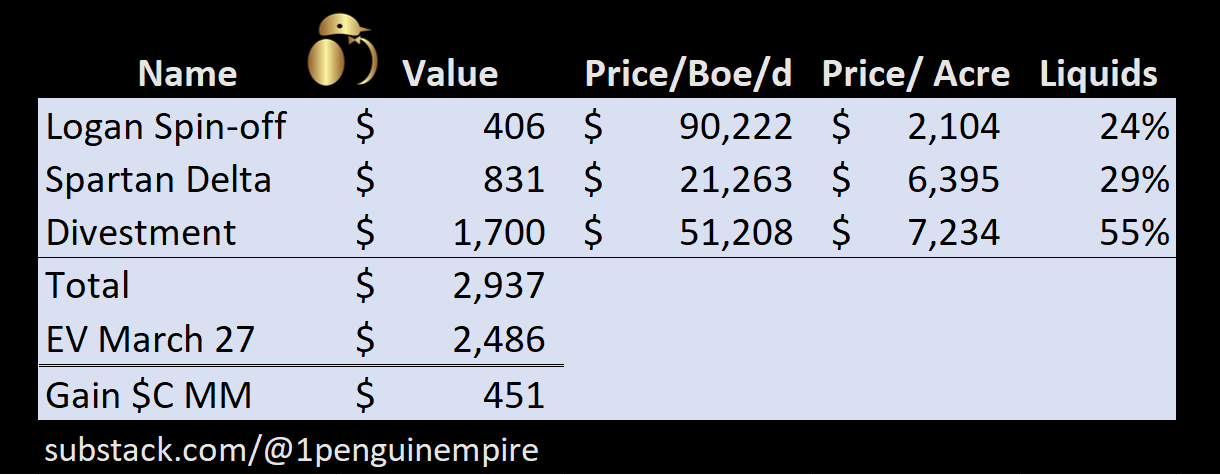

By the summer of 2023, Spartan Delta had, once again, entered into a sale of assets. As mentioned above, Spartan Delta split into three parts: 1. Logan Energy, 2. assets sold off to Crescent Point for C$ 1.7 billion, and 3. the remaining assets held by Spartan Delta. When Spartan Delta announced its financials for the period ending June 2023, Spartan Delta recorded on its income statement a GAIN of ~ C$ 549 million on the sale of its assets.

Not too shabby.

Before the re-alignment, Spartan Delta was worth approximately $ 2.49 Billion in enterprise value on March 27th (the day before the deal was announced). As of mid morning on August 10, 2023, the sum of the three parts is estimated to be worth C$ 2.9 billion, or an increase in value of ~ $451 million or ~18%. For comparison, shares of the XEG.TO energy EFT increased ~14.5% in the same time period.

However, perhaps the biggest benefit to Spartan shareholders was to monetize a large portion of those gains with a handsome C$ 9.5 dividend per share, plus 1 share in the new Logan Exploration, and 1 warrant for Logan shares. Plus, shareholders retained equity in Spartan Delta…

And Logan Energy was funded with approx. $109 million in cash to develop its acres.

The Logan spin off traded, ~ mid-morning on 8/10/2023, at around $90,000 per BOE/d (enterprise value). That seems high on BOE/d basis. Many other Montney producers trade in the $30s-40s k per BOE/d.

But, the Logan spin-off was granted approximately 193,000 acres of mostly undeveloped Montney, one of the most coveted oil and gas plays in North America. Now it’s true that the value of Montney land varies depending on its location, such as if it is in the gas part or the oil part of the play. But for reference, Pacific Canbriam purchased ~$47K of undeveloped Montney land for $130 Million in August 2022 to supply the proposed Woodfibre LNG project. That works out to $2750 per acre. Calima Energy provided a nice map of BC Montney land sales here (on P13). While this isn’t a straight apples-to-apples comparison, it can serve as a starting point. Especially since large tracts of undeveloped Montney land are becoming harder to find.

And, with the competition of the Coastal Gaslink pipeline, the on-going construction of LNG Canada at Kitimat, BC, and the Woodfibre LNG in the later stages of development planning, one can see why the market might give Logan an enterprise value north of $400 Million (stocks less cash), despite its small current production (~4500boe/d).

Based on Logan’s investor presentation (available here) management plans to spend ~ C$75 million in capital expenditures to grow production to 7000 boe/d by year end of 2023. They also plan to grow to 20K boe/d within 5 years.

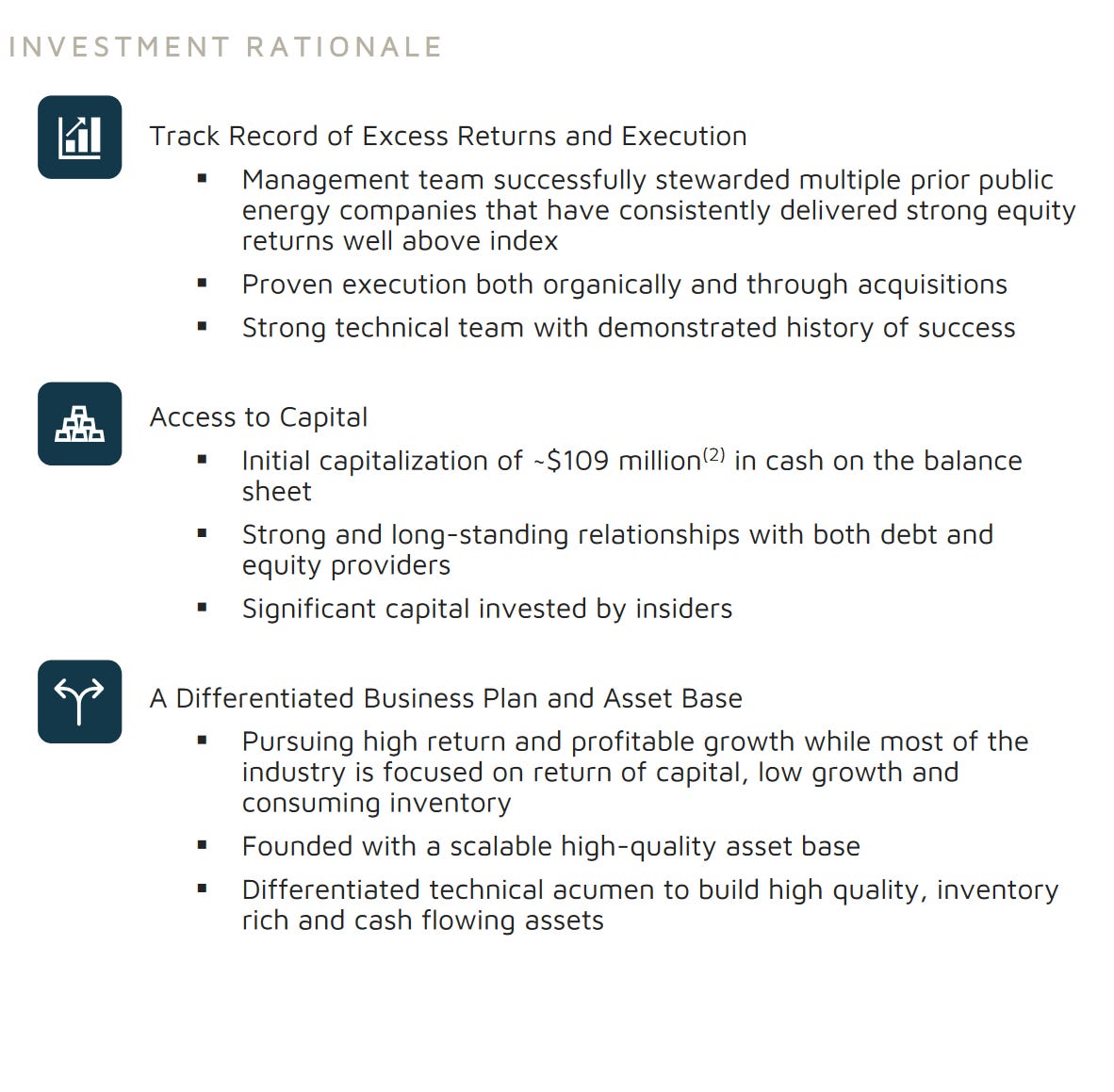

Below, you can see that Logan’s Strategy sounds a lot like The Spartan Way.

Management also claims to have a “differentiated Businesses Plan” in ‘pursuing high return and profitable growth while most of the industry is focused on return of capital…”

In closing, it is interesting to PenguinEmpireReports to see Spartan’s Group of Four, combined with other new additions to the team, set out ‘rinse-and-repeat” the Spartan Way. Only time will tell if they will be successful.

Thanks for Reading!

And …

KNOW WHAT YOU OWN before you buy.

https://static1.squarespace.com/static/5ebeb3beb8891c6346025774/t/645e9d7c632d0669e7e91f46/1683922301255/SDE+Q1+2023+Financials.pdf